Recently, I was reading up on the Global Fintech Ecosystem Report 2020 covered by Startup Genome and Crunchbase. Startup Genome is the world-leading policy advisory and research organization for governments and public-private partnerships committed to accelerating the success of their startup ecosystems. I have been reading their reports since 2018 and will usually read every report that I see in-depth. Here are some of their findings and my own thoughts.

Key Findings:

- The top 5 global Fintech ecosystems are Silicon Valley, New York City, London, Singapore and Beijing.

- Europe and North America no longer dominate the Top 20 Fintech ecosystems with APAC contributing as many globally leading hubs as North America.

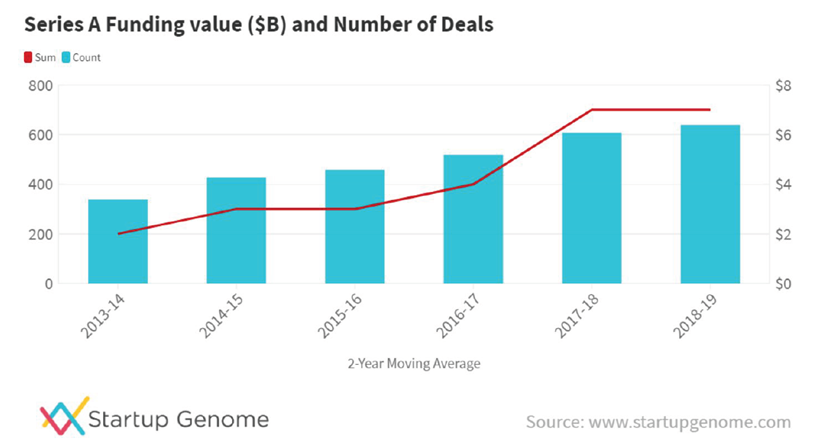

- Overall, the growth in Fintech funding is slowing down globally. Early-stage funding (pre-seed, seed and Series A) has plateaued almost everywhere. China in particular has seen a drop. The notable exceptions are Europe, and Americas (excluding USA), both of which have seen an increase.

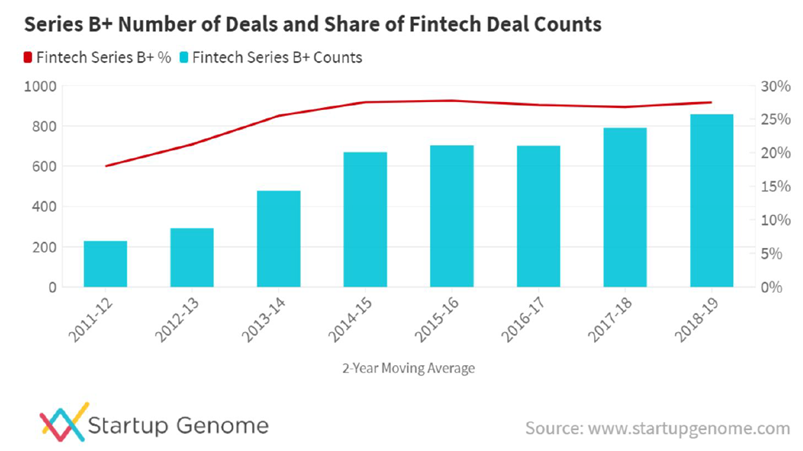

- Series B+ funding is doing better, with China being the only region down in 2019, but this is due to a whopper year in 2018, led by a $14B funding round for Ant Financial.

- The increasing share of series B+ rounds in total funding for fintech indicates industry consolidation with more money being poured into winners. This is ultimately necessary as Fintech commercials require large volumes for profitability.

- European Fintech funding continues its steady climb at all stages and with consistent unicorn growth, not the least reflective of rapid growth in user adoption since pandemic.

- Digital-only banking clearly is on the rise; including by adding new services such as wealth management as well as broader service bundles.

- Artificial Intelligence: A natural complement to Fintech, helping the industry develop hyper-personalized solutions.

- From competition to collaboration - incumbents and startup challengers increasingly realize the benefit in collaborating, resulting in a much larger number of partnerships between incumbent FIs and Fintechs as well as between non-financial players and Fintechs.

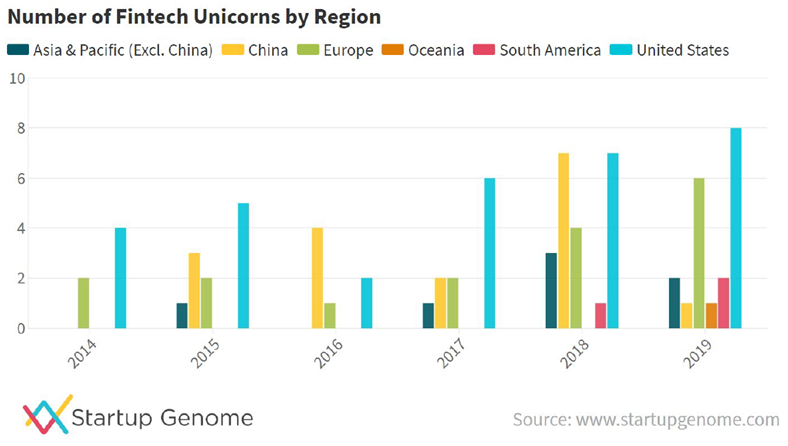

2018 has shown a record high of the number of fintech unicorns around the world. The increase was largely attributed to a bumper year in China, which became the first country to produce the same number of $1B+ companies as the US. However, the US has seen a steady increase in the number of unicorns produced each year, whilst 2018 seems to be an exceptional year for China. Also, it tends to be a case where Chinese Fintechs are typically focused on the domestic market, whilst US unicorns are often companies that aim for global expansion and domination. As a result, there is more scope for competition.

Overall, the growth in Fintech funding is slowing down globally. Early-stage (pre-seed, seed, and Series A) has plateaued almost everywhere. The median Seed round in 2020 (up to August) has not changed since 2019 and stands at $500,000 indicating that early-stage investors have become more selective. However, there is a significantly sharp increase in the number and sums of Series B+ deals that are done in the same period. This includes the mega venture funding round of Ant Financial’s $14B funding round amongst others. In Europe and the US, the increase in funding at Series B+ has been led by D2C digital banks with Chime, SoFi, Klarna, Oaknorth, and Nubank all receiving an investment of between $400-500M.

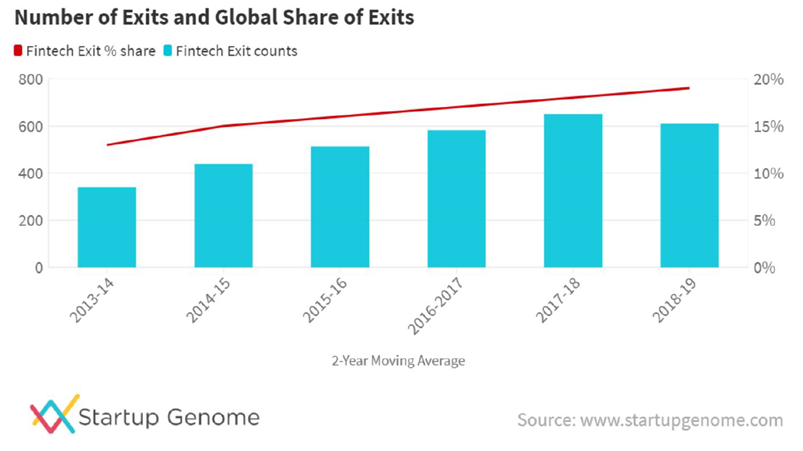

Despite the drop in exit counts, fintech has remained as a strong contributor to the global startup economy having delivered constant exit growth until 2018. Its share of overall exits has continued to increase in that time, and Fintech exits account for 19% of global exits across all subsectors in 2018-2019.

In terms of the various top tier ecosystems, we are also watching out for various up and coming ecosystems around the world.

Some of the ecosystems that we are watching for growth include Melbourne, Tokyo, Kuala Lumpur, Manila, Sri Lanka, Cairo, Kampala, Frankfurt, Nur-Sultan and Curitiba. These are the places that we expect to see more fintech unicorns coming out in the next 10 years to come.

I think fintech will see another round of revolution with the growing use of blockchain and artificial intelligence. Specifically, actuaries may be replaced by artificial intelligence in terms of deciding insurance premiums, interest rates for different clients based on their risk profile. I would also foresee a surge in terms of digital banks. Today, JP Morgan has its own digital banking division that serves the younger consumers (Wall Street meeting Silicon Valley).

Let's see... I still believe in the singularity.